Q: You said that the February cut was a reflection of Labor’s strong economic management. Are you disappointed that you didn’t see a cut today?

Jim Chalmers:

I try not to second guess decisions taken independently by the Reserve Bank. I don’t make decisions in advance and I try not to second guess them. One of the things that I implemented is that the Reserve Bank Governor gets an opportunity to talk the Australian people through their thinking and through their deliberations over the last couple of days at the Reserve Bank Governor. But I do think that the way that Labor has responsibly managed the economy, the way that this Government has been able to get inflation down and real wages up, keep unemployment low, keep the debt down, and the fact that interest rates have started to come down is a reflection on the progress that Australians have made together on our watch as a government. If you compare the economic situation now to three years ago, inflation was much higher and rising when we came to office. It’s much lower and falling now. And the fact that interest rates have started to come down is a reflection of that.

Q: Is the hold today a detriment to your election campaign?

Chalmers:

I don’t see this decision in political terms, and I’m sure that the independent Reserve Bank doesn’t see it in political terms either. We’ve already seen rates start to come down this year. That’s a very good thing. It’s a reflection of the progress that we’ve made together in the economy. And I don’t make predictions about the future. But I do remind people that there was almost no expectation whatsoever from the markets and from the economists today of a rate cut, but there is an overwhelming expectation of a rate cut in May, and in subsequent months. That’s the expectation of the market. I don’t get into those sorts of predictions.

DOGE-EE Dutton: Chalmers tries on a new Dutton nickname

Chalmers continues:

A vote for Peter Dutton is a vote for higher taxes, for no ongoing cost of living help, and for secret cuts to pay for his nuclear reactors. Now, every policy idea that he makes up on the run is only designed to distract from the fact that he doesn’t want to come clean on his secret cuts to pay for his nuclear reactors.

He says that the detail will come later, but we are now well into the election campaign, and Peter Dutton has still not come clean on his $600 billion in cuts that he needs in order to build these nuclear reactors which will push up electricity prices.

Now, today, he threatened cuts to school funding which was right from the DOGE play book. And we also know that he wants to Americanise Medicare as well, because when he was the Health Minister, he tried to gut and cut Medicare.

He said that the best predictor of future performance is past performance. When Peter Dutton was voted the worst ever Health Minister in our history, he tried to Americanise Medicare, and now we hear that he has in mind, cuts to education as well.

This is DOGE-ee Dutton, taking his cues and policies straight from the US in a way that will make Australians worse off.

And this Albanese Labor Government is getting inflation down, interest rates have started to come down, growth is rebounding solidly in the economy, unemployment is down, the debt is down as well. Real wages are growing in our economy.

So we are making welcome and progress in our economy together, but we know that there’s more work to do because the global environment is so uncertain, and people are still under pressure. That’s why our cost of living help as the centre piece of the budget is so important. It’s why it’s so important that we cut income taxes for every Australian taxpayer – not jack up taxes as Peter Dutton and Angus Taylor are proposing to do. Happy to take your questions.

Jim Chalmers is in his element here, as he talks about inflation and gives a bit of verbal side eye to the RBA board:

Rates have already started coming down this year and that’s a good thing. When we came to office, inflation and interest rates were both rising, and now, inflation and interest rates are both falling. And this reflects the progress that we’ve made together as Australians on inflation the Reserve Bank’s statement says that it has fallen and the continued decline in underlying inflation is welcome.

But they also make it very clear that they’re very focused on global economic uncertainty as well. Inflation was much higher and rising at the last election. Now, it is much lower and falling. Inflation was higher than 6% when we came to office, and it was rising fast. It peaked in 2022 – the year that we were elected.

And now, it is a fraction of what we inherited from Peter Dutton’s Coalition. It’s gone from 6.1% and rising before the election, and it’s now 2.4%, and underlying inflation is coming down as well. Now, we know that cost of living is front of mind for many Australians, and it’s absolutely front and centre in the budget I handed down last week. And it’s central to the big differences between the parties as well. Labor is helping with the cost of living, cutting income taxes for all 14 million Australian taxpayers, and strengthening Medicare at the same time.

The RBA seems very confused about how tariffs work and twisting itself to come up with a reason not to cut rates

In the RBA’s statement it said of the impact of Trump’s tariffs

On the macroeconomic policy front, recent announcements from the United States on tariffs are having an impact on confidence globally and this would likely be amplified if the scope of tariffs widens, or other countries take retaliatory measures. Geopolitical uncertainties are also pronounced. These developments are expected to have an adverse effect on global activity, particularly if households and firms delay expenditures pending greater clarity on the outlook. Inflation, however, could move in either direction.

But here’s the thing given Australia has ruled out retaliatory tariffs, Trump raising tariffs will not raise prices for Australia.

Let’s assume a worst-case scenario where the US puts tariffs on everyone and everything, but Australia does not retaliate with tariffs.

The biggest impact on prices will be in the US where prices for all its imports will rise.

Prices for US goods and services in other countries (apart from Australia) will also rise.

Maybe it will raise some of the input costs for stuff made in America that is then bought by Australians. But this is second or even third round effects, that are not likely to be strong.

So what else could happen? Well, a tariff war would likely cause the global economy to slow. What happens then? Well price rises slow because people can’t afford to buy things. So why is the RBA thinking this could be inflationary for Australia.

And here’s the kicker – an interest rate cut or rise has ZERO impact on prices that have changed due to a tariff. If a tariff raises prices by 25% the prices have gone up due to the tariff, not due to us all having more money and spending madly. So, what is the RBA thinking it is doing?

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.10 per cent and the interest rate paid on Exchange Settlement balances at 4 per cent.

Underlying inflation is moderating. [same subheading they had in February]

Inflation has fallen substantially since the peak in 2022, as higher interest rates have been working to bring aggregate demand and supply closer towards balance. Recent information suggests that underlying inflation continues to ease in line with the most recent forecasts published in the February Statement on Monetary Policy. Nevertheless, the Board needs to be confident that this progress will continue so that inflation returns to the midpoint of the target band on a sustainable basis. It is therefore cautious about the outlook. [This is rather weak. They have gone from wanting underlying inflation to be consistently within the target band, now they want to be confident about this. In February they had a whole paragraph about “However, upside risks remain.” That has been removed this month and yet… ]

The Board noted that monetary policy is well placed to respond to international developments if they were to have material implications for Australian activity and inflation.

The outlook remains uncertain. [same subheading they had in February]

Private domestic demand appears to be recovering, real household incomes have picked up and there has been an easing in some measures of financial stress. However, businesses in some sectors continue to report that weakness in demand makes it difficult to pass on cost increases to final prices. [Yes! Because we are struggling!]

At the same time, a range of indicators suggest that labour market conditions remain tight. Despite a decline in employment in February, measures of labour underutilisation are at relatively low rates and business surveys and liaison suggest that availability of labour is still a constraint for a range of employers.[ie – we think more of you should be unemployed because you might start wanting higher wages] Wage pressures have eased a little more than expected [ie oh you’re getting lower wages rises than we thought you would so errr gee better come up with a reason why this is irrelevant] but productivity growth has not picked up and growth in unit labour costs remains high. [Productivity is a weird thing for the RBA to care about for a rates decision. Productivity is a slow-moving long-term thing. A rate cut won’t affect it one way or the other and there will never be a quarterly change in productivity that would justify either a rate cut or increase.]

Deputy Governor of the Reserve Bank of Australia (RBA) Michelle Bullock speaks during Senate Estimates at Parliament House in Canberra

There are notable uncertainties about the outlook for domestic economic activity and inflation. The central projection is for growth in household consumption to continue to increase as income growth rises.[Given household consumption has been either flat or falling, this is not a big call] But there is a risk that any pick-up in consumption is slower than expected, resulting in continued subdued output growth and a sharper deterioration in the labour market than currently expected. [Gee, ya think? So the RBA here is giving a good reason to cut rates, and yet… guess they want to be cautious about… err the economy tanking??] Alternatively, labour market outcomes may prove stronger than expected, given the signal from a range of leading indicators.[The RBA not doing much to suggest they are just guessing – sure thing could be bad or could be good. But surely you can do a bit better than that?]

More broadly, there are uncertainties regarding the lags in the effect of monetary policy and how firms’ pricing decisions and wages will respond to the demand environment and weak productivity outcomes while conditions in the labour market remain tight. [Here the RBA is admitting it is not sure how long it will take for the rate cut of February to have an impact. If you are starting to think the RBA using a magic 8-ball to work out what is happening, you might be right]

Uncertainty about the outlook abroad also remains significant. On the macroeconomic policy front, recent announcements from the United States on tariffs are having an impact on confidence globally and this would likely be amplified if the scope of tariffs widens, or other countries take retaliatory measures. Geopolitical uncertainties are also pronounced. These developments are expected to have an adverse effect on global activity, particularly if households and firms delay expenditures pending greater clarity on the outlook. Inflation, however, could move in either direction. [again, very helpful. Thanks] Many central banks have eased monetary policy since the start of the year, but they have become increasingly attentive to the evolving risks from recent global policy developments. [essentially – some have cut because they raised rate higher than the RBA, and now they are wondering what the hell Trump might do]

Sustainably returning inflation to target is the priority. [same subheading they had in February]

Sustainably returning inflation to target within a reasonable timeframe is the Board’s highest priority. This is consistent with the RBA’s mandate for price stability and full employment. To date, longer term inflation expectations have been consistent with the inflation target and it is important that this remain the case.

The Board’s assessment is that monetary policy remains restrictive. [ie we are still thinking that the current interest rate will cause more people to lose their jobs, and we like that] The continued decline in underlying inflation is welcome, but there are nevertheless risks on both sides and the Board is cautious about the outlook. [we are scared to do anything because life apparently is not certain]

The Board will rely upon the data and the evolving assessment of risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board is resolute in its determination to sustainably return inflation to target and will do what is necessary to achieve that outcome. [come back in May when we will cut rates and no one will accuse us of being political]

Australia Institute view: Interest rate hold more political than the cut we should have had

Today’s decision to keep interest rates on hold is just as political as if the RBA had cut rates.

And a second cut – from 4.1% to 3.85% – is exactly what the Reserve Bank should have delivered today.

The Treasurer and Prime Minister constantly remind us that the bank is independent of government and politics.

Now, suddenly, the RBA doesn’t want to look political.

“Australian mortgage holders are suffering too much for the bank to tiptoe around the sensitivities of our political leaders,” said Greg Jericho, Chief Economist at The Australia Institute.

“When rates were going up, the bank had no problem slugging borrowers ten times in a row.

“Now that rates are coming down – and the bank board is meeting less often – the RBA is more worried about appearing political than doing the right thing by Australians.

“All the indicators have continued to move in the right direction since the last rate cut. Underlying inflation has now been below 3% for three straight months – so why wait?

“Interest rate cuts never happen as a one-off. The RBA has already indicated that more are coming. So, I repeat, why wait?”

Greens MP Adam Bandt has been in Perth (which is one of the target seats for the Greens) where he has appealed to the people of WA to think about their vote.

The Greens had a very good state election, taking the balance of power in the legislative assembly, and getting about twice the vote of the Nationals. And this is despite a massive counter campaign about protecting the fossil fuel industry.

Bandt:

In the seat of Perth, if less than one in ten people shift their vote to the Greens, then Sophie Greer can be the next member of Parliament.

As we head towards a likely minority Parliament, that puts the voters of Perth in a really powerful position to keep Dutton out and get Labor to act by getting dental into Medicare, by wiping student debt, and by taking real action on the housing and climate crisis.

Two thirds of people in Perth are in housing stress. We’ve got people who are skipping meals because they can’t afford to pay the rent. The price of groceries is soaring. People know we can’t keep voting for the same two parties and expecting a different result.

Here in Perth, the local member is a patsy for the gas corporations, is quite happy with the status quo where one in three big corporations pays no tax, and meanwhile, everyday people struggle. This election if you want change, you can vote for it. Perth can be in the box seat, by getting a Greens representative in the middle of Parliament.”

When it comes to the Coalition’s housing policy, Bandt said it would only make housing prices increase (which our research bears out)

[His] plan is for first home buyers to have to pay more for their homes, and take out bigger mortgages that they’ll struggle to afford.

It is not an answer to the housing crisis.

We’ve got to ensure the government starts building homes that first home buyers can actually afford, and make the banks offer low-rate mortgages at rates people can afford.”

Victoria, like much of Australia, is one of the richest places in the world and can afford anything it decides is a priority. Victoria can build a rail loop, a train to the airport, a bunch of other things and the sky will not fall in.

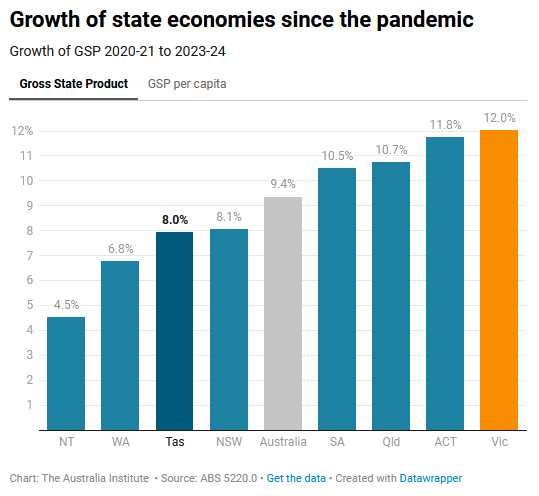

Victoria’s economy has grown faster than the rest of the country since the pandemic:

The Victorian Government’s books are not in bad shape:

This doesn’t mean everything the Victorian Government wants to build is a good idea. All government spending should be backed by clear, robust analysis, something that has been lacking from some of the Vic infrastructure proposals. But the idea that Victoria can’t afford to build more major infrastructure isn’t right.

Having addressed the ridiculous idea that the Chinese navy might somehow cut the Sydney-Perth underwater cable, let’s look at the cables connecting Australia with the rest of the world, for which Dutton and various commentators breathlessly ring alarm bells.

If an adversary does decide to cut a cable, the most stupid way to do so would be to cut it right on Australia’s doorstep, rather than doing sabotage at a safe distance, somewhere along the thousands of kilometres’ length of one such cable. (You’d think as a former police detective, Dutton would be attuned to how criminals’ think.)

It would be difficult for Australia to defend the full lengths of all these cables in any case – and you can’t do worse in attempting to protect them by planning for only 6 to 8 incredibly expensive submarines, which may or may not arrive by mid-century. And are we all suppose to forget that Australia would still have satellite communications in the unlikely event of losing ALL of its communication cables?

Leave us a message

Loading form…

SubscribeThe biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

Loading form…